You might not even notice it, but chances are you’re losing money every time you use your normal bank or credit card while traveling internationally.

Legacy banks are simply awful when it comes to using them abroad.

They charge extra for using ATMs in other countries.

They give you foreign currency at a totally unfair exchange rate.

They add hidden fees.

With some banks, it’s like daylight robbery!

When I was a permanent nomad, I once calculated I was losing hundreds of Euros in exchange fees every year.

Luckily, there are now new types of travel debit cards that let you avoid many fees and get a fair currency exchange rate. They also have mobile apps with features that can be very helpful to travelers.

Why use travel debit cards?

There are many reasons why pre-paid debit cards are ideal for international travel.

Mind you, we’re not talking here about credit cards best for getting Airmiles and other rewards while you’re spending at home. These debit cards will instead give you low fees when you are abroad.

The advantages of a travel debit card include:

- Lower fees abroad. Normal banks or credit cards often charge higher transfer fees, exchange rates, withdrawal fees, and other hidden costs.

- Easier to monitor. Debit cards that are good for traveling let you check recent transactions or get notifications in real-time using an app. This is especially great for avoiding scams, fraud, and checking on sketchy ATMs in developing countries.

- More secure. You can easily block a travel debit card with one tap in the app. You can also pre-charge your debit card with smaller amounts, so if your card gets hacked or stolen, the thieves can’t raid your entire checkings account. (It’s happened to me!)

- Travel-specific benefits. Cards such as Revolut add in little extras that are super useful to travelers, such as automatic travel insurance (based on your phone’s geolocation) or free access to airport lounges.

While there are numerous debit cards available, I’m personally a big fan of Revolut, Wise, and N26.

If you’re traveling often or for a long time, it makes sense to sign up for several of these debit cards. This lets you combine their monthly fee-less ATM withdrawal limits, plus gives you several back-up cards in case of theft or loss on the road.

Best debit cards for travelling

Wise (formerly TransferWise)

Recommended!

![]()

Wise (formerly known as TransferWise) is one of the most established mobile banking platforms that cater to travelers. It’s also one of the most transparent companies when it comes to rates and fees.

You get a Wise debit card after opening a Wise Borderless Account. With Wise you can hold or convert money in more than 50 currencies. This includes major currencies but also minor ones, like, say, the Sri Lankan Rupee or Moroccan Dirham.

You can convert your USD, EUR, AUD, or whatever into local currencies at favorable exchange rates ahead of time, so you don’t have to rely on exchange in the destination. Or you can let Wise take care of it automatically when you use the debit card. Wise’s exchange rates are lower than many banks.

Wise also operates via a mobile app, letting you monitor transactions or freeze the card with one tap.

With the Wise debit card, ATM withdrawals are free up to $250 per month. Signing up is also free and there are no monthly or annual account fees.

If you plan to temporarily work abroad during your travels, Wise can be very useful to have. Along with the debit card, you also get local bank details for a range of currencies. So you can do a backpacker job in Australia and get paid in Australian Dollar to an Australian bank account number and receive it on Wise, where you can convert it for cheap to anything else.

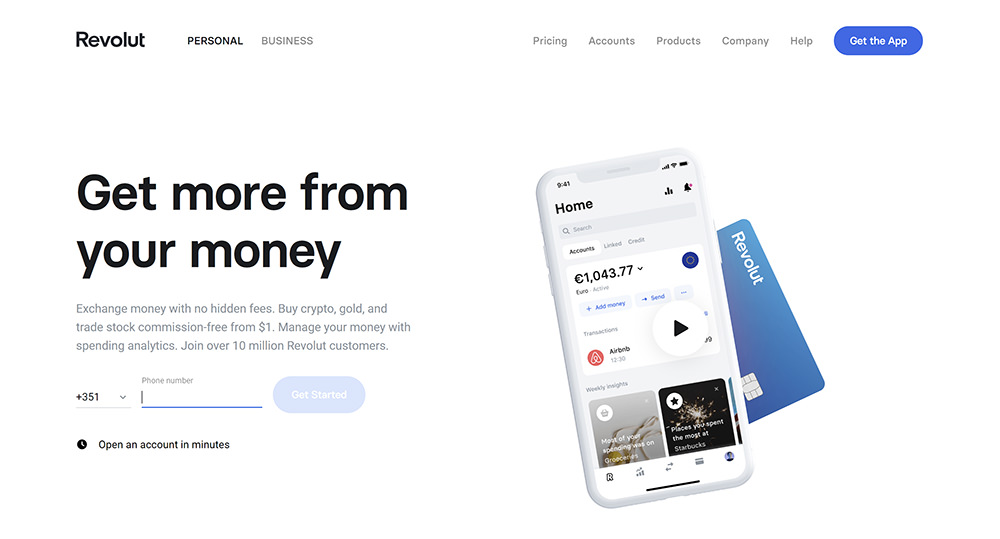

Revolut

Revolut pairs a mobile app with a physical travel debit card. What makes Revolut one of the best debit cards for foreign travel is that it also has several traveler-specific bonus features on the paid tier cards.

But firstly, Revolut gives you access to spend in over 150 currencies. Secondly, Revolut offers fee-free spending and ATM withdrawals up to a specific limit. You can get free ATM withdrawals for up to $300 per month and a small fee of 2% for anything over the limit.

The app lets you easily categorize expenses and set budgets, which is great for keeping tabs on your travel spending. It’s also great for couples traveling together as it has a very useful Split Bill function.

Revolut has several account types, with standard (suitable for most travelers) being free. You can view the different Revolut plans here. The paid tier gives you travel insurance, which it calculates automatically on a per-day basis using the geolocation from your phone. It also gives you fee-free ATM withdrawals up to $600 per month, and LoungeKey Pass access (over 1000 airport lounges worldwide).

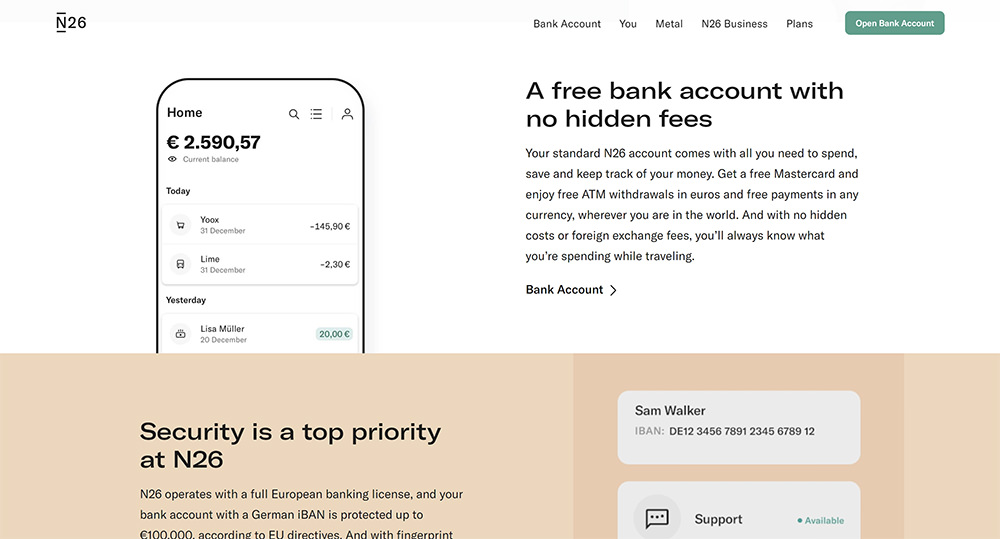

N26

N26 is a mobile banking platform founded in Germany that is now used worldwide by travelers. While making your usual payments, you can take advantage of cashback and travel discounts offered by N26.

The N26 travel credit cards work in sync with its user-friendly mobile app — the app sends you real-time alerts about your account activity. In case your card gets lost or stolen, it also includes the ability to lock your account.

The best part about N26 is no hidden fees. N26 has no minimum account balances, no maintenance fees, and no insufficient funds fees. You’ll be spending a lot more money on travel and pleasure instead of fees.

N26 also allows you to withdraw money locally at ATMs with no fees in the US, Canada, Puerto Rico, Australia, Mexico, and the UK.

Travel debit card comparison

Travel debit cards are best for managing your money effectively while traveling as opposed to collecting miles and points for travel. With the fee savings and convenience that they offer, it’s a great alternative to your regular banks.

Below is a comparison of the three bank cards mentioned:

| Wise | N26 | Revolut | |

| Open an account | FREE | FREE | $0-$14.99/mon |

| Monthly account fees | FREE | FREE | FREE |

| Transfer money rate/ Convert currencies | Real exchange rate | Rate based on Visa (subject to change) | Interbank exchange rate (0.5% over $6500) |

| Monthly ATM Withdrawals | FREE up to $250 (2% over $250) | FREE in select countries (2% Out-of-network ATMs) | FREE up to $300 (0.5% +2% international ATM fee) |

| Adding Money | 0.2% (direct debit) | FREE | FREE |

As you can see, each of these cards offers fee-free ATM withdrawals up to a certain amount each month. Since the cards are free to sign up for, you could get all of them and spread your travel funds across these cards.

One advantage of doing so is that if someone hacks your bank card, they won’t get access to all of your money. This actually happened to me a couple of years ago in Honduras, where I lost over $4000 through fraud that took many months to get back. That’s not a problem if each card only has a few hundred Euros or Dollars on them at any given time, to be topped up from your main bank account or credit card whenever necessary.

The other advantage is that you can use each card up to the monthly limit and not pay any ATM fees.

Other travel banking options

The debit cards above I’ve listed because of their benefits but also because they accept customers in many different countries. (Some debit cards are still available only in one country, such as Starling in the UK.)

Besides these debit cards with apps, there are also regular banks you can sign up to that are beneficial to travelers. Some smaller independent banks promote themselves by not charging for foreign withdrawals. In the United States, Charles Schwab bank has a checking/debit account that doesn’t charge ATM fees abroad. In the United Kingdom, the smaller Metro Bank offers a similar deal.

Signing up for a whole new bank account only makes sense if you’re going to travel a lot. Otherwise, it’s easier to sign up right away for one of the debit cards mentioned above.

Some links may be affiliate links, meaning I may earn commission from products or services I recommend. For more, see site policies.

{kind=link}

I’ve been in Puerto Vallarta for 4 months. My bank is a credit union in Oregon. My wallet was lifted at Walmart 3 wks ago. My bag was on my shoulder. A lady bumped my cart and started rapidly apologizing, while a guy reached into my bag and took my wallet. Had all my cards w/me as I was going phone shopping. I know, dumb on several levels. I only realized what happened when texts for purchase approval started pouring in. Yeah for security aps! So…Credit union would send new debit card to home address only.

My daughter (who banks there too) wasn’t allowed to pick it up. If I changed address, no plastic can be sent for 30 days! Andi had to wait for new card then send it down ($60). Felt like I was 7 instead of 70. I had no access to my money except by xfering it to her acct and her sending it to me via West U. By the way, Chase V sent my new credit card o/n at no charge! What a lesson! I’m signing up for travel cards today. Thanks so much Marek.

Still Livin & Learnin! Billie B

Ooof, that sounds like quite an ordeal! I recognize the feeling as I once had to travel several months in South America just using Western Union after I lost my bank cards… not ideal. Glad you got a new card though and are getting some backup ones too!

Hi Marek,

Great travel page. You’ve done a lot of work and I really like it. I am commenting also to let you know (and other) that the cool travel debit cards you have advertised aren’t available if you live in Japan. Just so you know.

Thanks for the travel tips!

Scott

Ah that’s a bummer! I tried to pick ones that have rolled out at least in North America and Europe but I guess they aren’t truly global yet

I used Starling ( an Internet based phone App ) bank in southern Africa and all around Europe. They cover any currency, any country, they charge no fees and their exchange rate is very close to interbank.

Note this is a proper bank, via a phone App, not just for travel card. The debit card they provide is a Mastercard which can be an issue in some countries ( like Zambia). Security is high and the road can be locked from your phone. I ma very happy with them.

Good tip! I didn’t include them for now as they are still specific to the UK but I heard great things about Starling. 🙂